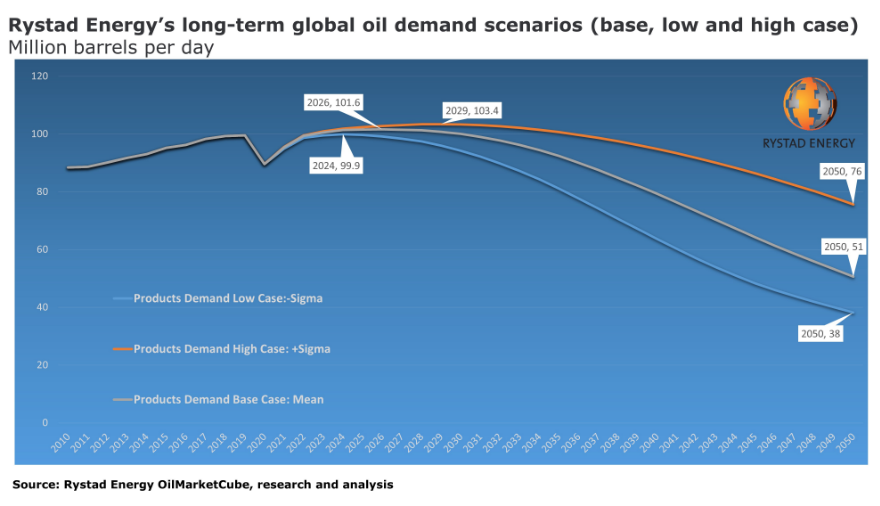

The adoption of electrification in transport and other oil-dependent sectors is accelerating and is set to chip away at oil sooner and faster than in our previous forecast. As a result of this transition, Rystad Energy is downgrading its peak oil demand forecast to 101.6 million barrels per day (bpd), a pinnacle that will come in 2026, earlier than thought, plateauing before falling below 100 million bpd after 2030.

In our updated base case, which we call the “Mean” case, oil demand will be whittled away mainly by a growing electric vehicle (EV) market. Aside from the staggering takeover of EVs, assumptions across all our scenarios (low-case, mean-case and high-case) see oil demand being either phased out, substituted, or recycled across a range of sectors.

We forecast tectonic shifts – some sudden and others slowly evolving – in plastics recycling, a growing share of hydrogen in the petrochemical sector, and oil substitution in power, agriculture, and maritime sectors. Other sectors will still see thriving oil demand in the mid-term, such as trucks, maritime and petrochemicals, and aviation in the long term, where we see a sizable substitution of jet fuel with non-petroleum fuels such as bio-jet fuel, which is still part of the overall liquids products universe.

"Oil demand will evolve in three phases. Through 2025, oil demand is still affected by Covid-19 impacts and EVs are still slow to take off, then from 2025-2035, structural declines and substitution impacts -especially in trucks - take hold, and then finally, towards 2050, the recycling of plastics and accelerated technologies in maritime will be the final transition leg bringing oil demand further down towards 51 million bpd in 2050 in our Mean Case," says Sofia Guidi Di Sante, oil markets analyst at Rystad Energy.

Road transport (passenger vehicles, buses and freight), which makes up over 48% of oil demand, will be the ultimate driver of the transition. The swiftest transition is already well underway in the electric passenger vehicle sector, which currently makes up 6% of global vehicle sales, but will account for 23% by 2025 and then accelerate towards 96% penetration by 2050.

Read Related Articles

- Oil Markets Face Uncertain Future after Rebound from Historic Covid-19 Shock

- IEA: Petrochemicals Set to be the Largest Driver of World Oil Demand

- U.S. Energy Information Administration Releases Annual Energy Outlook 2018

- Shell to Cut Jobs and Capacity at Major Singapore Refinery

- Refiners Worldwide Struggle With Weak Demand and High Inventory

Trucks, which account for 18% of total demand, will not electrify in the short-term, but when the adoption occurs in the mid-2030s and begins reaching critical mass, the substitution impact will be much higher on a per-unit basis compared to smaller vehicles that use less fuel. EV trucks will benefit from the technology groundwork already being established in passenger vehicles. Buses will also see a gradual transition from petroleum diesel to electric and biofuels. The EV truck market share will rise to 6% in 2025, 21% in 2030, and 61% in 2040.

Petrochemicals, which make up 14% of total oil demand, are expected to grow until at least the mid-2030s as plastics consumption per capita grows worldwide. The demand then peaks as plastics recycling rates converge towards 75-80%, as observed in glass and metals, from the current effective rate of 5%, at the same time as hydrogen-sourced feedstock picks up from less than 1% today to 30% of the virgin petrochemical feedstock for LDPE, HDPE, PP and PVC plastics production in 2030.

Maritime, which makes up 6% of demand, is expected to be dominated by oil for at least through the mid-2030s, after which we expect to see switching to LNG, hydrogen, electric batteries, and other carbon-neutral vessels, especially in newbuilds. This sector already underwent a big transition with IMO 2020, which saw the switching from high-sulfur fuel to ultra-low sulfur fuel.

Aviation, which makes up less than 7% of oil demand, is expected to continue to grow until 2050 as no viable oil substitution technology exists. The gradual introduction of bio-jet fuel will limit pure kerosene jet fuel demand growth but will not affect the strong upward trajectory in aviation through 2050, unless a viable alternative technology is introduced.

Other sectors (agriculture, energy own use, own energy use, industry, buildings, and power generation) continue a downward sloping trajectory. Growing agriculture and energy own use demand partially offset the accelerated decline of oil consumption in power.

Alternative Scenarios

The scenario Rystad Energy considers as most likely is the Mean case. However, we also provide two alternative scenarios, a high-case and a low-case, which represent reasonable upside and downside probabilistic range from our mean case. All three scenarios are lower than our previous oil demand scenarios released in October 2020.

In the low case scenario oil demand peaks at 99.9 million bpd in 2024 and demand then declines almost three-fold to 38 million bpd by 2050. In the high case scenario, oil demand peaks at 103.4 million bpd in 2029 and declines more gradually to 76 million bpd by 2050.

“We expect Covid-19 behavioral impacts to spill over through 2025, as we see the work-from-home trend persisting even after the lifting of lockdowns, keeping downward pressure on transport fuels. Although oil demand is expected to recover above pre-virus levels, it will be just marginally. Any post-pandemic oil demand boom is tempered by structural declines that were already ongoing long before the virus, such as substitution in power, industry, and buildings,” Guidi Di Sante concludes.

Our previous base case was released in October 2020 and was projecting oil demand to peak at 102.2 million bpd in 2028. Before Covid-19, we had called for peak oil demand of just over 106 million bpd in 2030.

For more analysis, insights and reports, clients and non-clients can apply for access to Rystad Energy’s Free Solutions and get a taste of our data and analytics universe.

About Rystad Energy

Rystad Energy is an independent energy research and business intelligence company providing data, tools, analytics and consultancy services to the global energy industry. Our products and services cover energy fundamentals and the global and regional upstream, oilfield services and renewable energy industries, tailored to analysts, managers and executives alike. Rystad Energy’s headquarters are located in Oslo, Norway with offices in London, New York, Houston, Aberdeen, Stavanger, Moscow, Rio de Janeiro, Singapore, Bangalore, Tokyo, Sydney and Dubai. For more information, visit www.rystadenergy.com.

Comments and Discussion

There are no comments yet.

Add a Comment

Please log in or register to participate in comments and discussions.